International Business & Economics Studies (IBES) is an international, Refereed, double-blind peer-reviewed, open-access journal published by Scholink. The journal aims to provide a high-level platform for scholars and researchers all over the world to share latest findings and views in the field of Business & Economics Studies. We would welcome scholars and researchers engaging in the related field to submit your manuscripts which are complete unpublished and original works and not under review in any other journals to IBES. Both of online submission and E-mail submission (ibes@scholink.org) are acceptable. ------------------------------------------------------------------------------ The journal includes, but is not limited to the following fields:

----------------------------------------- Index/List/Archive

Open access: International Business & Economics Studies is available online to the reader "without financial, legal, or technical barriers other than those inseparable from gaining access to the internet itself." Peer review: International Business & Economics Studies takes peer review policy. Peer review is the evaluation of work by one or more people of similar competence to the producers of the work (peers). | |

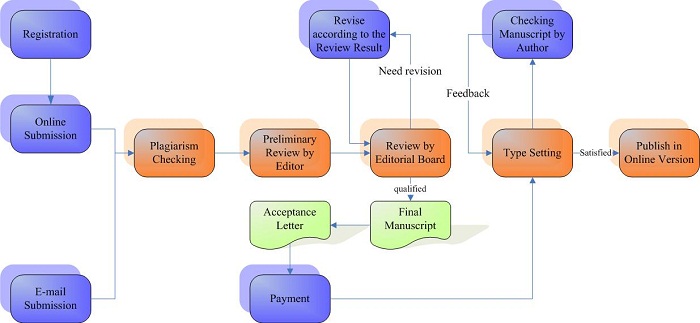

Journal Publishing Flowchart

Announcements

Call for Original Papers: Vol 8, No 2, June 2026 |

|

| We are calling for submission of papers for Vol. 8, No. 2, June 2026 (Deadline: June 24, 2026). Please submit your manuscripts online. You may also e-mail submissions to ibes@scholink.org If you are interested to be a reviewer, we welcome you to join us. Please download and finish the application form at http://www.scholink.org/doc/Application%20Form%20for%20Editorial%20Board%20Members.doc Then send the completed application form to the editor: ibes@scholink.org. Please pay attention to the basic requirement to reviewer: 1. Possess a doctorial degree. 2. Research area is relative to the subject of journal. 3. Proficiency in English. We also would like to cooperate with other institutions to publish special issues. To publish a special issue, please contact with the editor ibes@scholink.org

|

|

| Posted: 2018-12-06 | |

| More Announcements... |

Vol 8, No 3 (2026)

Table of Contents

Articles

|

Congying Guo

|

p1

|

|

ZhiPeng Cao, XiaoLi Bai

|

p16

|

|

Yang Zhou

|

p30

|

|

Qiuchen Zhang

|

p40

|

|

Chunyan Mo, He Huang, Xianzai Yu

|

p56

|

|

Shuxia Kong, Ke Zhang, Xu Liu

|

p72

|

|

Zhijun Zhou, Liu Yanhong, Xianfu Wu, Fang Liu, Jiexia Li

|

p102

|

|

Ren Wenjing

|

p137

|

|

Jian Li, Fuqi Liang

|

p145

|

|

He Luxing

|

p165

|

|

Ke Ni

|

p181

|

|

Tingfei Che

|

p196

|

|

SHEN Xiaoxia, XUE Jianbo, WANG Ting, LI Rongxiang, WANG Kaixuan

|

p221

|

|

Mei Li

|

p230

|

|

Tang Ning

|

p254

|

|

Rui Pang

|

p264

|

|

Jianghua Deng

|

p273

|